The Balance Sheet

Today on MBA Mondays we are going to talk about the Balance Sheet.

The Balance Sheet shows how much capital you have built up in your business.

If you go back to my post on Accounting, you will recall that there are two kinds of accounts in a company's chart of accounts; revenue and expense accounts and asset and liability accounts.

Last week we talked about the Profit and Loss statement which is a report of the revenue and expense accounts.

The Balance Sheet is a report of the asset and liability accounts. Assets are things you own in your business, like cash, capital equipment, and money that is owed to you for products and services you have delivered to customers. Liabilities are obligations of the business, like bills you have yet to pay, money you have borrowed from a bank or investors.

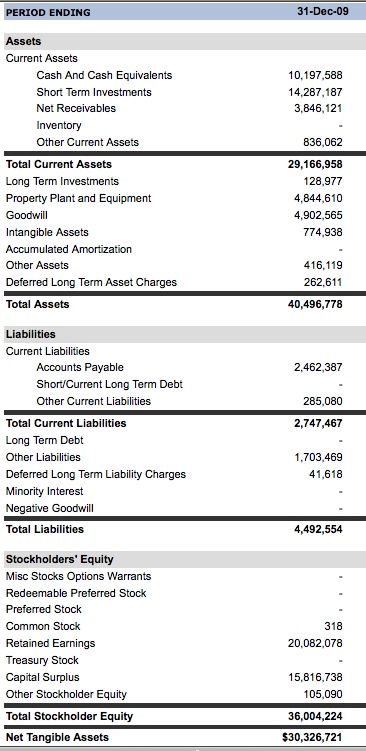

Here is Google's balance sheet as of 12/31/2009:

Let's start from the top and work our way down.

The top line, cash, is the single most important item on the balance sheet. Cash is the fuel of a business. If you run out of cash, you are in big trouble unless there is a "filling station" nearby that is willing to fund your business. Alan Shugart, founder of Seagate and a few other disk drive companies, famously said "cash is more important than your mother." That's how important cash is and you never want to get into a situation where you run out of it.

The second line, short term investments, is basically additional cash. Most startups won't have this line item on their balance sheet. But when you are Google and are sitting on $24bn of cash and short term investments, it makes sense to invest some of your cash in "short term instruments". Hopefully for Google and its shareholders, these investments are safe, liquid, and are at very minimal risk of loss.

The next line is "accounts receivable". Google calls it "net receivables' because they are netting out money some of their partners owe them. I don't really know why they are doing it that way. But for most companies, this line item is called Accounts Receivable and it is the total amount of money owed to the business for products and services that have been delivered but have not been collected. It's the money your customers owe your business. If this number gets really big relative to revenues (for example if it represents more than three months of revenues) then you know something is wrong with the business. We'll talk more about that in an upcoming post about financial statement analysis.

I'm only going to cover the big line items in this balance sheet. So the next line item to look at is called Total Current Assets. That's the amount of assets that you can turn into cash fairly quickly. It is often considered a measure of the "liquidity of the business."

The next set of assets are "long term assets" that cannot be turned into cash easily. I'll mention three of them. Long Term Investments are probably Google's minority investments in venture stage companies and other such things. The most important long term asset is "Property Plant and Equipment" which is the cost of your capital equipment. For the companies we typically invest in, this number is not large unless they rack their own servers. Google of course does just that and has spent $4.8bn to date (net of depreciation) on its "factory". Depreciation is the annual cost of writing down the value of your property plant and equipment. It appears as a line in the profit and loss statement. The final long term asset I'll mention is Goodwill. This is a hard one to explain. But I'll try. When you purchase a business, like YouTube, for more than it's "book value" you must record the difference as Goodwill. Google has paid up for a bunch of businesses, like YouTube and Doubleclick, and it's Goodwill is a large number, currently $4.9bn. If you think that the value of any of the businesses you have acquired has gone down, you can write off some or all of that Goodwill. That will create a large one time expense on your profit and loss statement.

After cash, I believe the liability section of the balance sheet is the most important section. It shows the businesses' debts. And the other thing that can put you out of business aside from running out of cash is inability to pay your debts. That is called bankruptcy. Of course, running out of cash is one reason you may not be able to pay your debts. But many companies go bankrupt with huge amounts of cash on their books. So it is critical to understand a company's debts.

The main current liabilities are accounts payable and accrued expenses. Since we don't see any accrued expenses on Google's balance sheet I assume they are lumping the two together under accounts payable. They are closely related. Both represent expenses of the business that have yet to be paid. The difference is that accounts payable are for bills the company receives from other businesses. And accrued expenses are accounting entries a company makes in anticipation of being billed. A good example of an accounts payable is a legal bill you have not paid. A good example of an accrued expense is employee benefits that you have not yet been billed for that you accrue for each month.

If you compare Current Liabilities to Current Assets, you'll get a sense of how tight a company is operating. Google's current assets are $29bn and its current liabilities are $2.7bn. It's good to be Google, they are not sweating it. Many of our portfolio companies operate with these numbers close to equal. They are sweating it.

Non current liabilities are mostly long term debt of the business. The amount of debt is interesting for sure. If it is very large compared to the total assets of the business its a reason to be concerned. But its even more important to dig into the term of the long term debt and find out when it is coming due and other important factors. You won't find that on the balance sheet. You'll need to get the footnotes of the financial statements to do that. Again, we'll talk more about that in a future post on financial statement analysis.

The next section of the balance sheet is called Stockholders Equity. This includes two categories of "equity". The first is the amount that equity investors, from VCs to public shareholders, have invested in the business. The second is the amount of earnings that have been retained in the business over the years. I'm not entirely sure how Google breaks out the two on it's balance sheet so we'll just talk about the total for now. Google's total stockholders equity is $36bn. That is also called the "book value" of the business.

The cool thing about a balance sheet is it has to balance out. Total Assets must equal Total Liabilities plus Stockholders Equity. In Google's case, total assets are $40.5bn. Total Liabilities are $4.5bn. If you subtract the liabilities from the assets, you get $36bn, which is the amount of stockholders equity.

We'll talk about cash flow statements next week and the fact that a balance sheet has to balance can be very helpful in analyzing and projecting out the cash flow of a business.

In summary, the Balance Sheet shows the value of all the capital that a business has built up over the years. The most important numbers in it are cash and liabilities. Always pay attention to those numbers. I almost never look at a profit and loss statement without also looking at a balance sheet. They really should be considered together as they are two sides of the same coin.

Comments (Archived):

I have been following Google’s balance sheet for ~3 years now for the purposes of multiple comps we do. Not once during those years did I ever see a dollar of debt.Obviously GOOG has a mountain of cash, so there’s I suppose there’s no reason to take on debt since they can’t even invest their own cash, but it seemed surprising to me to me nonetheless that they’ve never touched any form of debt… Can’t they invest in their business at a greater return than the cost of capital, particularly consider how cheap capital is right now with banks borrowing essentially for free?

they may have borrowed some money in the early days to finance capex. i don’t know to be honest. but since they went public, and probably before it, they’ve been able to finance their business with their own cash which is certainly the best and safest way to go if you can

Very nice explanation of the most important items on the Balance Sheet. MBA Mondays has become one of the highlights of my week.Are you planning on going into more detail on the concept of Working Capital? You kind of touched on it on the Current Liabilities vs. Current Assets discussion, but I think it’s so important it needs its own post.I’m looking forward to the post on financial statement analysis!

yes, absolutely. it will be a full blown post

so the retained earnings is the bonuses and stock allowed to employees and the capital surplus goes to stockholders in the end ? Do I get that right ?Great MBA mondays as always !

not exactly. retained earnings are cumulative profits that have not been dividended out to shareholders

then can retained earnings be considered cash? or do they ever work their way to the cash line on the balance sheet?

yes, they can become cash or other assets like property plant and equipment

Fred, it’s worth pointing out that units are thousands of US dollars, basic and obvious though it might seem. That’s how we get from:10,000,000 + 14,000,000 on the balance sheet to 24 *billion* in your discussion.The sound start you’ve made to MBA Mondays reminds me of something a smart and good business-school teaching colleague once said. It was along the lines of: there are three courses you really need. Financial statement analysis. Ethics. And… sorry, I forget the third. It’s probably the course where they teach you not to waste pearls of wisdom on absent-minded friends.

ethics is so important in businessway more than financial statements

Great: we can look forward to a “moral Monday” in your MBA series!

“The cool thing about a balance sheet is it has to balance out.”Somewhere my former accounting professors are smiling.

+1

+1

Another great post, Fred – thanks. If you would allow me to pick on a point you wrote:”” If you compare Current Liabilities to Current Assets, you’ll get a sense of how tight a company is operating. Google’s current assets are $29bn and its current liabilities are $2.7bn. It’s good to be Google, they are not sweating it. Many of our portfolio companies operate with these numbers close to equal. They are sweating it. “”While it is true that Google is not sweating it, I think its also important to point out that asking a company to find ways to increase its working capital (i.e. current assets minus current liabilities) may not necessarily be a good thing for it’s profitability ratios.For anyone that’s interested, this discussion on the pros and cons of increasing working capital may be useful:http://www.finance30.com/fo…

“Hopefully for Google and its shareholders, these investments are safe, liquid, and are at very minimal risk of loss.”I’m not sure about safe, but don’t items categorized as “short-term” investments have to be able to be liquid in a year? Same with short-term debt. According to GAAP, I think both have a year window.

Cody,You are right that “short-term” investments typically have to be considered liquid at most within a year. However, with the complexity of today’s investment market, you sometimes get investment vehicles that may have “seemed like” or “marketed as” a short term investment, when in reality, they are not.A good example was Auction Rate Securities – a debt instrument where interest rate were regularly reset through a dutch auction (usually every x number of days) – which some of the money market or short term investment accounts were used to invest in to generate a higher interest for the customers. Although it was considered highly liquid (and marketed as short-term investments) when it was first introduced, the wide-spread auction failure in 2008 resulted in many company’s inability to gain access to these funds. Many companies ended up having to re-class these investments from ST to LT on their balance sheet until the matters are resolved.You can read more about what happened if you Google it 😉

One point I thought you would have mentioned (I believe you blogged about it back in the day) is real estate leases. They are off-balance sheet, but usually represent the largest real liability startups have. And tons of vc/investor energy went into renegotiating these after bubble 1.0 burst. Worst thing any entrepreneur can do is take a long-term lease — can kill you.

good point Al. probably worth a whole post at some point on MBA Mondays

Depending upon your accounting policies, the current year’s lease obligations are typically accounted for on the balance sheet. The current year of long term liabilities only not the full obligation of the lease.In a complete set of financial statements, a schedule is typically appended which lays out the long term real estate obligations and the calculation of the short term or current year element which is included on the balance sheet.A couple of pointers on diminishing your exposure on real estate leases:1. Do not enter into long term leases but rather a fairly short initial term with a series of renewal options. As an example do not enter into a 15 year lease but rather a 3 year lease with 4 3-year renewals. You can pull the plug at any renewal time.2. Incorporate in every lease — in the defaults and remedies section — a provision for liquidated damages in the event of tenant default rather than an open ended liability. I typically try to get 6 months rent as liquidated damages in the event of default. This defines your downside.3. Try to include a termination provision in the event of any foreseeable catastrophe — change in the law, loss of funding, death of the founder, etc. I am routinely able to negotiate such provisions.4. Know that in most bankruptcy cases, you may revoke leases with no real recourse. That is typically the law in most states and in Federal bankrupcties. Again, you can reject a lease.5. Your actual legal damages in most states is limited to NPV of your contractual rent MINUS the NPV of a replacement tenant. Things like leasing commissions and tenant improvements make it a bit more complicated. Take heart that your liability is NOT just the full amount of the rent. Most states require a landlord in the event of a default to mitigate its own damages.5. Make the dispute resolution technique binding arbitration rather than simply real estate common law as arbitration is less costly and will likely protect you in the short term from precipitous actions by a landlord. Never get near a Court if you can instead have binding arbitration.6. Never agree to a contractual or statutory landlord’s lien on your property on the leased premises. Never, ever, ever.7. Visit w/ your landlord annually. Don’t let things get to the blood in the streets before you start talking. Every landlord in America will take half of the rent while you work out your problems.

JLM – great post and response. Key point for me is 1) – never enter into long term leases. I would also add from an entrepreneur’s point of view, wait until your eyeballs are bleeding to get bigger digs. Yes there will be discomfort, but better that that living with too big an obligation that dominates your view of the business. Of course, once you’re profitable, on the right trajectory can be a bit less conservative, but you’re back to point 1.Great comment!

To make your real estate dollar go as far as possible, use open office partitions (cubicals) and make your first limited growth move to putting some discreet internal operation in outside space.Get an expansion option in the same building or a right of first refusal on any vacant space. If the landlord cannot accomodate your growth, get the right to terminate your lease early.For every possible real estate dilemma, there is a solution. An easy solution.

Another great entry in the series. Best thing since Brad Feld & Jason Mendelson’s Term Sheet posts, IMHO.One small question: is the Net Tangible Assets number at the very bottom the Total Stockholder Equity minus the Goodwill and Intangible Assets (and something else, since that doesn’t add up)? In your experience, is that number present/important on a startup’s balance sheet?

net tangible assets is their word for stockholders equity

I definitely remember my teachers repeatedly stressing that a balance sheet must balance. As simple as it sounds it is very revealing to how healthy the business really is. I’m looking forward to your post on cash flow as that is the real meat of understanding a business at the points where P&L and BS are interacting. One thing that could be said about balance sheets is how they differ from P&Ls in that BS are a snap shot in time while P&Ls are a statements of activity over a period. One of the best uses of a BS is looking at several to see trends which is what you will get into with the cash flow statement. The funny thing with bankers is that we almost always review a balance sheet first and then look at the P&L. Contrast this with business owners typically spending the most time on the P&L. The BS shows the structure of a business and helps you make assumptions as to what the P&L should look like. Great series and looking forward to more.

Educating folks on reading financials is great! The more difficult part of it though definitely starts to show in this discussion of the balance sheet.The Notes to the Financial Statements are so, so integral to the understanding of the balance sheet. For example, defining “net receivables” (likely it’s net of allowance for doubtful accounts).I’ve heard it said, always look at The Notes because that’s where the bodies are buried.The balance sheet can be deceptive. Not all debt is created equal. Not all equity is created equal. Classing of something as debt and/or equity can become a real challenge.Looking at the liquid assets side, same thing. What’s included in ST investments, for example, plays into the “unpleasantness” of the last few years. Something may appear liquid, but that can change given a market upheaval.Don’t be fooled by looking at the numbers in isolation.

“always look at The Notes because that’s where the bodies are buried.”- very true

“… always look at The Notes because that’s where the bodies are buried.”I love it! 🙂

I could not possiblly agree more — the Notes, the Notes, the Notes as well as the assumptions related to the accounting policies incorporated in the financial statements are everything.

As a supplement to MBA Mondays, some may be interested in checking out the financial topics on the Khan Academy website. He’s got a couple of videos on the balance sheet. Also other videos specific to venture capital.

I took an summer accounting course at the university here a few years ago, MBA Mondays has been a good recap for when I’m starting to need to really keep track of things, so thank you. :)Oh, and my silly guess on why Google uses “Net Receivables” instead of “Accounts Receivables” is probably as simple as Google’s an internet company and the accountants are having some fun! 🙂

Hey there Fredland, first-time commenter, many-year reader. This series of posts is so wonderful and so useful and so helpful. I am so grateful for your work and even more so for the community (JLM comes to mind!) who expands on every one of the MBA Monday posts.I got inspired by you indirectly to learn accounting and so I am taking a class at a local LA college this semester (we are currently learning how to make closing entries).Each blog post of yours is at least if not more valuable than 3 hours of instruction from the professor–and certainly a lot more real-world!I’m especially looking forward to your financial statement analysis because I just read Ben Graham’s book on the subject and it’ll be nice to see balance sheets of Google analyzed rather than balance sheets of Bethlehem Steel!—And just to join the MNK fun, I’d like to add that as we expand into an economics of abundance, what’s waiting right around the door are the ETs. Yes folks, Star Trek and the Interstellar Alliance are about to become very real.

This is helpful, Fred, thank you. Together with 10 other volunteers, I adjudicate Operating Grant applications for our municipal-level arts funding program (~$2.2million), and always rely on the accountants in the group to help me understand an organization’s balance sheets, its expense and revenue projections, and so forth. Your post makes me a tad more literate here. Proof that the non-profit sector can benefit from these MBA Mondays posts, too!

I have been a regular reader of this blog for the last 8 months or so but have yet to submit a comment. That said, I have a comment about the direction of the Monday posts. Although I am not sure how my knowledge base compares to some of the other frequent contributors, I have found that the MBA Monday are pretty elementary and pushing ahead slower than I had expected (closer to undergrad business Mondays). I think the section is a good idea, I was just wandering if anyone else expected more out of the posts and if not, just wanted to voice my opinion. (I think that the section in its current state would make for a popular independent blog)

The balance sheet is only the beginning for what can become a very illuminating view of the business’s guts.I would urge folks to keep a running spreadsheet and graphs over time of a number of different RATIOs.Look at the typical liquidity ratios (current ratio, quick ratio, cash ratio) as well as financial leverage ratios (gross profit margin, return on assets, return on equity) — this will require you to look at both the income statement and the balance sheet. This is the glue which binds the present snapshot w/ the longer term view.Another exercise which I highly recommend is a quick snapshot liquidation analysis — if you had to liquidate the enterprise what could you hope to realize. This is where things like capitalized tenant improvements and goodwill evaporate into the ether.I highly urge you to keep a handle on your ratios as they are often the leading indicators of your initial success (or failure).

Isn’t net receivables A/R less bad debt, and a pretty normal way of looking at A/R?

I’d like to see the GAAP rules changed to make the writing off of Goodwill on acquisitions mandatory over a period of time. It is effectively a balancing number and should come out over time. Google carrying something like $1B or whatever of Goodwill for the acquisition of YouTube is an accounting anomaly.

Fred,A related balance sheet point is Good Will is subject to an annual test for impairment. These amounts would also be in the Balance Sheet Notes. Great Article!

Nice work Fred. Thanks for the great MBA Mondays series – very educational.For those masochists out there who would like to learn more about Goodwill see Warren Buffett’s enlightning discussion of Accounting Goodwill vs Economic Goodwill: http://www.berkshirehathawa…

The MBA Monday posts, you don’t comment on much. You soak it in, and you wait for another day to let the comment horses run again. 🙂

As someone else said, net receivables is usually A/R less allowances for bad debt, no real funny games afoot, just shorthand (unless the relationship between A/R and allowances was off the chart). Google’s also adding in deferred taxes and income tax receivable to the total as well. I’m not an accountant nor did I stay at a Holiday Inn Express last night, but lumping in deferred tax assets with accounts receivables seems odd–I’m sure it’s standards friendly if GOOG’s doing it, but this exceeds my MBA 1.0 familiarity with accountancy.http://yahoo.brand.edgar-on…

Hi Fred, do you know where I can obtain an investment memo that would walk us students throught he analytical framework that VCs go through in analyzing an opportunity? If you can point me to the format and even a sample one, that would be great. Thanks