How To Calculate A Return On Investment

The Gotham Gal and I make a fair number of non-tech angel investments. Things like media, food products, restaurants, music, local real estate, local businesses. In these investments we are usually backing an entrepreneur we've gotten to know who delivers products to the market that we use and love. The Gotham Gal runs this part of our investment portfolio with some involvement by me.

As I look over the business plans and projections that these entrepreneurs share with us, one thing I constantly see is a lack of sophistication in calculating the investor's return.

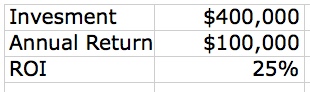

Here's the typical presentation I see:

The entrepreneur needs $400k to start the business, believes he/she can return to the investors $100k per year, and therefore will generate a 25% return on investment. That is correct if the business lasts forever and produces $100k for the investors year after year after year.

But many businesses, probably most businesses, have a finite life. A restaurant may have a few good years but then lose its clientele and go out of business. A media product might do well for a decade but then lose its way and fold.

And most businesses are unlikely to produce exactly $100k every year to the investors. Some businesses will grow the profits year after year. Others might see the profits decline as the business matures and heads out of business.

So the proper way to calculate a return is using the "cash flow method". Here's how you do it.

1) Get a spreadsheet, excel will do, although increasingly I recommend google docs spreadsheet because it's simpler to share with others.

2) Lay out along a single row a number of years. I would suggest ten years to start.

3) In the first year show the total investment required as a negative number (because the investors are sending their money to you).

4) In the first through tenth years, show the returns to the investors (after your share). This should be a positive number.

5) Then add those two rows together to get a "net cash flow" number.

6) Sum up the totals of all ten years to get total money in, total money back, and net profit.

7) Then calculate two numbers. The "multiple" is the total money back divided by the total money in. And then using the "IRR" function, calculate an annual return number.

Here's what it should look like:

Here's a link to google docs where I've posted this example. It is public so everyone can play around with it and see how the formulas work.

It's worth looking for a minute at the theoretical example. The investors put in $400k, get $100k back for four years in a row (which gets them their money back), but then the business declines and eventually goes out of business in its seventh year. The annual rate of return on the $400k turns out to be 14% and the total multiple is 1.3x.

That's not a bad outcome for a personal investment in a local business you want to support. It sure beats the returns you'll get on a money market fund. But it is not a 25% return and should not be marketed as such.

I hope this helps. You don't need to get a finance MBA to be able to do this kind of thing. It's actually not that hard once you do it a few times.

Comments (Archived):

Fred, this is very good and straightforward.The only thing I’ll add is a simple investment break-even point (payback period) analysis so that the investor can figure out at a glance how long their initial capital will tied up and when the business will become profitable.

that’s a great point. for these kinds of investments, i like to see a fairlyquick payback period. i like to structure them with a high initial profitshare (like 50%) and a lower profit share once the capital has been paidback.

Makes a lot of sense.I assume that’s because these are non-tech investments. In tech, where the growth velocity can be a lot faster, I would assume that you would prefer the dividends to be reinvested.Side note: I think it’s great that you guys are helping small businesses in this way (capital + advisory). This is part of what makes America great. We need more of this in the UK.

there is very little in common between what we do at Union Square Venturesand what the gotham gal and i do with these investments. as you point out,the USV investments are about growth and building large scale businesses.our personal investments are much more about backing a small business thatwe think ought to exist. in those, we are focused on payback and cash flowreturns

love it when you do these kind of posts

thanks

how seriously do you take these types of projections? to me financial forecasting for startups seems especially difficult. perhaps it is just me but i definitely don’t know how any entrepreneur can do it with any type of confidence/certainty. as an investor, do you find these types of projections to be useful?

yes, because these are simple businesses often operated by serialentrepreneurs who have done it before. i agree that the kinds of investmentsthat USV makes are much harder to project

Ahh serial entrepreneurs explains the basis for trust. But drawing an extrapolation curve feels like fabrication to me. As long a it’s plausible and defended with some facts about why performance will be in the ballpark of prediction it has some value.I guess if someone can sell you a curve of the future they can sell customers on the idea as well 🙂

This explains a lot, thanks. I missed this point in the original post, and was just about to start bashing about the 10 year thing.

Ask any engineer, extrapolation is hogwash. Even interpolation between known boundary points are just limited estimates.Get some data, make up a curve or estimate that matches investor expectations and get to work. How accurate are these predictions.Housing market, 2k tech bubble, etc

Financial projections are like getting a prostate exam.It is not something you relish doing.It is not something you should overlook doing.If you fail to do it, you may regret it.There are no really good alternatives.

So financial prediction “specialists” know the insides and out of a$$ets, and have great senses of humor. Got it

Hmmm, I never thought of it that way. LOLPerhaps, financial projections like prostate exam data are all pulled out of one’s…………..? LOLIn humor is truth. Or is that wine?

In vino veritas (and very true, which is why many late-stage UK interviews involve a trip to the pub )

I couldn’t agree more. Without a basic expense and projected income spreadsheet, you can’t function.Or more accurately, if you aren’t projecting your expenses you aren’t running your business.Revenue projections are always a guess but I was brought up with the high/low/likely model as well. If you don’t do this cash flow is a surprise which is inevitably a bad thing.Thnx for pounding this home with clarify JLM.

Wow, this is a very scary question.”Zero based budgeting” — the ability to construct a proforma budget for a start up business is the life line of any start up. While it is a painstaking exercise, it is fundamentally very easy to do.How does one eat an elephant? One bite at a time.How does one construct a budget? One line at a time.The expense side of the equation is far easier than the revenue side of the equation. The expenses are exactly what you should expect to run any business. Having said that, it is still a lengthy process to get it right but if you concentrate on one area (e.g. compensation) at a time, you can wade through it with confidence.I like to see budgets made which document all the assumptions separately so one can simply change the assumptions and develop a quick “sensitivity analysis” of how the results differ.I always like to see a set of projections — high, low, likely — as opposed to a single projection and ensure that the deal is attractive through the width of the chalkstripe.I like my forecasts to be updated on a quarterly basis, so that over time the likely outcome becomes more obvious as the real numbers begin to impact the projected numbers. I call this process “wiggling in on the truth”.I think this is an area in which experienced VCs and modestly inexperienced entrepreneurs should use an “exemplar” — the format of the very best financial projection in one’s stable. This adoption of a “best practice” approach ensures that there is a consistent approach to forecasting and begging for money.This is also an area in which a young entrepreneur would do well to self-medicate — ooops, I meant self-educate — by getting a mentor or experienced entrepreneur to take a look at the projections BEFORE you are making your first real pitch.One last comment — use tabloid sized paper in landscape mode so that you can see the entire life of the investment at one fell swoop.

Thanks JLM, great advice, and greatfully taken.The range of expected curves shows many regions which help frame a problem. Wiggling in on the truth is analogous to tracking (you continually update your estimate of true state with each measurement).Predicting fixed costs is a good start for would be founders. I know I need a design pro for look/feel, and help with metrics and sales, finance/books, and legal costs of incorporating. These are fairly predictable costs.Predicting revenue/user growth is ok within an order of magnitude (I know I won’t get more than the Twitter market on my site within a year). But anything finer is fiction/guessing.

Not to be too cynical about this but once you have the expense side of the equation done and complete, you test your revenue assumptions by matching your projections to the expected rates of return necessary to get the investors to “yes”.This is why a range of projected outcomes — high, low, likely — is important. If the deal works anywhere within the continuum created by superimposing these curves on each other, then the deal likely works.While nobody bats 1000, there are an awful lot of home runs, triples, doubles and singles hit. But you never really know until you swing.

Fair enough.

Revenue predictions, in my experience, for a tech start up (or biotech for that matter) are really like waving a finger in the air. They are not even educated guesses. Particularly in years 3 and beyond when most people really start to ramp up the revenue.I’d like to know how much attention Fred pays to the financial forecasts, particularly the revenue element, that he sees when people approach him for backing at USV.

I like to lowball expectations, to give me some breathing room and more importantly to shock the heck out of people when I can over deliver.My magic 8 ball isn’t quite good enough to predict users, revenue, with anything more than wishful thinking. At the moment, I’m a little tunnel visioned on building a tool I can really use, so it has a good chance of traction.

expense projections are important to me in our USV investments. revenue projections are meaningless until the business starts to have revenues.

Certainly, predicting revenue accurately, IMHO, is close to impossible for most startups. However, it can give you a good idea about the mindset of the owners. Are the conservative? Aggressive? Realistic? Just completely out of it?

It’s not necessarily about the numbers themselves, even though those are important. When an entrepreneur presents these numbers, questions will invariably follow. What is the overall size of the market? How do you assume you will achieve the gross margins in this analysis? What are the factors that could disrupt your market?Financial forecasting is certainly art and not science. As a financial analyst myself, I’ve put plenty of these analyses together to know how important assumptions are to the overall analysis. If the business team cannot answer the questions coming from the analysis, then they do not know their business and will not get funding.Simply put, the logic behind the numbers and the ability to answer questions are probably more important. This is why an experienced analyst, business coach, or entrepreneur looking at your numbers would be invaluable.

I can project with great certainty how much money I will spend. I can project with some confidence how much money I will bring in.But, for the life of me, I’ve never been able to project when I’ll go out of business or sell the company.

It will be a Thursday.

and it will be a sale 🙂

As you pointed out, this method is more suitable for investments with predictable cash flow.I like these type of posts: would love to hear more about VC-maths/venture investment evaluation.

Realize that this doesn’t apply to your theories on bigger business, but..I like the way of thinking about businesses as transient entities. I wish more web tech businesses would accept this reality. The only lasting, sustained effects a business can have are the social/business value it generates during it’s existence. My hockey stick pitch curves are going to show a flattening and drop off estimate relevant to a current tech. The tools I’m building now will be replaced by superior versions by myself or others, or the market will move on.Hah, good luck to me finding investors. “yeah this product will be obsolete in 5 years tops. I aim to be the one who continually disrupts my own market until it approaches free”.

From the man with the plan, Steve Blank mentioned 3 years might be a better horizon.”Regardless of whether a company is in a new market, an existing market, or a resegmented market, the one certainty is that within three years the company will be faced with a competitive challenge. The challenge may come from small competitors grown bigger, from large companies that now find the market big enough to enter, or from an underlying shift in core technology. Facing these new competitive threats requires all the resourceful, creative, and entrepreneurial skills the company needed as a startup.”

he is right

The startup culture is infiltrating larger organizations. Very groovy trend.

Thanks for the post Fred.

I’ve been doing ROI projections on a real estate project I’m evaluating. I’m having trouble adjusting for time value corrections though. My first stab looked like what you present in this post, but this ROI doesn’t account for changes in the value of money itself. Would it be enough to take the future value of the future cash flows and use those rather than the 100k in the example?Second, I would like to add to the suggestion above of calculating the break-even point that you need a break-even point _including opportunity costs_. Break-even in the sense of ‘when do I make today’s dollar amount of my investment back’ is sort of interesting but what you really want to do is compare against an alternative investment, even if it’s just a savings account with compounding interest. Solving this in Excel is not obvious though, at least not to an Excel amateur like myself, so I ended up writing a small C++ simulation and used bisection to approach the solution.This being said, I once thought I could make a great product out of a simulation software package that would do exactly what I described above to calculate the ROI of solar panels, but I never even managed to explain to any of the people who I thought would be my customers what the whole idea behind it was :/

the best way to do that is take the IRR and then subtract the assumed rate of inflation over the life of the project and then you’ll get a “real rate of return”

Agree completely.One note about real estate as a class of assets.”Make the trend — the inflation trend — your friend.”Inflation is a great bonanza to real estate. A “normal” rate of inflation — say 2-3% annually — is what creates phantom equity in real estate.Buy and hold good quality real estate for 15-30 years (long enough to get beyond the imposition of a single business cycle like today).Finance it prudently using the repayment of debt as a proxy for the creation of financial equity. As the debt goes down, your equity goes up.At the end of the mortgage life, you have no debt — it is all now your patiently repaid equity paid for by your tenant’s rents.On top of that you get to reap the benefit of the inflation at 2-3% for 30 years, that is going to be OK.Oh, yeah, then do a tax free exchange.

What do you mean by ‘phantom equity’ in this post?

I was alluding to the invisibility of equity or value which is built up in real estate by repaying debt. As debt is paid down, the equity value (not as a defined accounting term, mind you) increases while the market value is also hopefully increasing.When you pay off the mortgage over 15-30 years, the debt is completely extinguished and the entire value is your equity though you never really saw it increasing from year to year.Real estate is working for you when you are sleeping.

Ok I see, thanks.

Institutional real estate (pension funds, pension fund advisors, insurance companies, etc) has a well accepted financial analysis approach. While it may differ just a bit from entity to entity, it is essentially a 15-year discounted cash flow with a Year 0 investment (this is an important distinction as your investment dollars flow in at the BEGINNING of the year and your Year 1 returns are typically received at the END of the year) and a Year 15 sale (residual value).Rental revenue assumptions are made on a proforma or actual lease by lease basis as well as capital inflows for tenant improvements, renovation and operating expenses (institutional real estate typically is NNN — tenant pays the taxes, insurance and utilities and CAM (common area maintenance)).Expenses are painstakingly projected based upon comparable properties or the actual property’s operating history. You can get a bit of guidance from BOMA — building owners and managers association.You have to budget vacancy and leasing commissions and tenant improvements during the life of the real estate investment.The big decision point is the rate of increase on future rental assumptions. Of course, every developer in the history of the world thinks rents go UP forever. Not so but over 15 years — highly likely. This is why they use 15 years. It flattens out the market vagaries and allows inflation to work its magic.This is a good disciplined approach even if you are buying a duplex.If you are investing with a developer the typical deal structure is 25% equity commands a 7-10% cumultive preferred return and 50% of the profits. Financial performance should be audited and if off by 3% the audit gets paid for by the developer otherwise the cost gets split.

Lots of good info here – I would only add that a lot of institutional quality real estate is not NNN (although a lot is) but instead the tenant pays for increases in expenses over some fixed amount. The owner still has inflation protection on the expense side for the life of a lease.One note on the inflation point – this is applicable provided the property is financed with fixed rate debt.

A NNN lease and a Base Year w/ the pass through of annual expense increases after the Base Year are financially identical over the term of the lease. In the Base Year approach, one has included the first year expenses in the initial rental rate.I also dislike the administration of Base Year leases because they always cause confusion between the initiation date of the lease and the calendar year of the expense administration. Messy accounting.Having leased literally tens of millions of SF of space, I always want to be quoting a NNN rental rate when the competition is quoting a higher Base Year rental rate. The lower number — even when it is only a bit of faux alchemy — usually commands the better reception in the market.Inflation is still the BFF of real estate regardless of whether it is financed using fixed or floating rate debt.In my view, it would be folly to finance real estate long term with floating rate debt ever. The small increment that is required to obtain fixed rate debt is almost always worth it. If for no other reason than the ability to sleep better. That is a cost of debt issue not an inflation issue.Remember that most of the trendy focus on floating rate comes from when long term fixed rate debt mandatd “pre-payment” penalties which were quite onerous. Lenders had match funded their obligations with the mortgage payments and were vexed if you toppled their finely organized world.Folks were seduced to a bit of arbitrage using LIBOR floating rates which have been historically a good bet and will be a good bet in the future when capital markets calm down again.LIBOR was, oh, so sophisticated! Kind of like French cuffs.The secret of real estate finance — there are NO secrets!

One scenario where the NNN and base year economics can differ is if you have declining expenses, rarely the case, however it’s cropping up now with lower tax resets driven by sales prices well off the highs of a few years ago. Some lease expenses are now well below their base years.I think the argument for real estate as an inflation hedge is mostly an argument for “real estate, prudently levered, is a good long term investment.” Perhaps a discussion for another time.

Hmmm, not really.A NNN lease passes along the actual property taxes to the tenant. If they vary, the pass through varies. The tenant only pays the actual property taxes.A Base Year lease sets a base year which includes the property taxes for that base year. If the property taxes decline — as in your scenario — then the tenant receives a credit for the decline in the property taxes thereby receiving a credit against the property tax amount included in the base year calculation. The credit is applied against the “increases” or the next month’s rent.In both scenarios the tenant only pays the actual property taxes.While I agree that the property tax issue is theoretically going to be an important touchstone in the immediate future, both NNN and Base Year leases contemplate this eventuality and ultimately deal with it fairly and consistently.

The key is if taxes decline below the base year, since there are no negative escalations in a gross lease. Assume a $20 net rent, $6 in operating expenses, $6 in taxes. This is equivalent to a $32 gross rent. If taxes go to $7, the tenant with the gross deal pays $32 + a $1 escalation, and the NNN tenant pays $20 + $6 + $7. Equivalent at $33. However, if taxes go to $5, the tenant with the gross deal still pays $32, while the NNN tenant pays $20 + $6 + $5 = $31.

Let’s get our nomenclature right first.Net (NNN) lease — tenant pays Base Rent plus all operating expenses including property taxes, insurance, utilities and CAM (common area maintenance) as Additional Rent. This is the gold standard amongst institutional quality real estate owners.Base year lease — tenant pays Base Rent which includes the base year property taxes, utilities and CAM and pays for the changes in the preceding costs as Additional Rent. Fairly infrequent amongst institutional quality real estate owners.Gross lease — tenant pays Base Rent and all expenses are included in that Base Rent. Archaic lease format and all protections accrue to the benefit of the tenant. Very rare in institutional quality real estate.The Gross lease is irrelevant to our conversation as there is no expense pass through of any kind.The NNN lease is also irrelevant as there is a complete expense pass through all the time.The base year lease provides that the tenant pays the “changes” in the expenses. The flaw in your argument is that there are routinely “negative escalations” in a base year lease. Why? Because sometimes expenses go down after the base year — in particular CAM expenses which are very, very dependent upon the local economy.Institutional quality leases always include a provision to compel a landlord to protest the property taxes and to pass along the benefit of any property tax reduction to the tenants less the cost of the protest. In many instances, the tenant can both compel the landlord to protest the property taxes but can also directly undertake the burden of protesting the taxes itself and pass the cost back to the landlord if they are successful. When you say “…there are no negative escalations in a gross lease…” you are mixing the concepts of a gross and a base year lease and you are simply wrong.In a CBD high rise office building, I can assure you that your big law firm tenants, in particular, and sophisticated tenants, in general, are all over the pass throughs and the property tax issues.I did not invent net, base year or gross leases but I have done a million of them.

This really shouldn’t be that attractive of a topic for me. But I admit to enjoying learning about these details. It makes me want to start renting, just so I can protest tax increases and lower my monthly fee. Speaking of taxes, I should look into my home’s property tax increases. It’s sky rocketed in the 12 years since I moved in.The predictability of the system over a 15 year time span may be the appealing factor. Even in a wildly fluctuating market, inflation will win the day, and real estate investments will reap the rewards.

Real estate is a funny business because everybody is in it whether they are an owner or a tenant. Remember real estate works 24/7 even if you don’t.

Thanks for the information, it’s refreshing to find ‘beyond amateur’ advice on the web.My situation is quite unusual, in that I’d be the developer (4 unit building) myself and finance it with 25% of my own money and 75% from a mortgage. Of course that would mean I’d get to keep 100% of the profits.Furthermore re: the fixed/floating rate, the difference in my country (in Western Europe) is is about 2 pct now (averages are just under 3% for a yearly renewable vs just under 5% for a 30 year fixed); on top of that, by law, floating rates can never more than double. Basically at this point, if I can negotiate the yearly floating down just a little bit, I am already sure that I will never pay more anyway than what I would if I’d take a fixed rate now. (there are intermediate options like 5 or 10 year fixed but the interest hike is non-linear). Just saying, in circumstances like this, it can pay to take a floating rate, and with hardly more risk than with a 30-year fixed rate.

You have it figured out perfectly. Good luck. Thi sis a great time to be investing in real estate.

I like the way that problem turned into a nicely organized methodology. No interest in real estate investment, but I certainly appreciate a solid framework.

I’m with kidmercury on the quality of the projection if the ROI isn’t properly understood and calculated. Do any of your entrepreneurs use an accountant/financial advisor who can help them with their model? As someone who’s done this in the past, I see a opportunity but convincing an entrepreneur to pay (even a below typical CPA/market rate) for this is difficult.

i do a lot of pushback, error correction, and QC as part of our diligence on these personal investments. i think that is often better than hiring a CPA

This is likely why they bring you the deals in the first place.

2 things : you don’t seem to take any discount over the cash flows. I think it makes sense to add some risk factor (based on the business and the visibility). Obviously, the risks of a small local store is quite low, yet, you may want to assume that the expectation of $100 has greater chances to be met initially than later.Also, for local stores (but maybe I’m not too familiar with NYC’s market), the biggest asset is “intangible” : the goodwill (not sure about the term) : it’s the right to sell goods/services there, as well as the location, the existing market… etc. I think this has value even if the business dies and should probably kept as a residual value to be added to the last cashflow. What do you think?

i don’t like to take the discount in the analysis. i like to take the result and compare it to the “discount” i would apply or even subtract that discount and make sure there is still a return beyond the discount expected

Alternatively you can risk-weight the cash flows as opposed to adding the “risk-factor” to a discount rate or discounting the final value. One way is to blend an upside and downside case.

Calculating the IRR (internal rate of return) is, in effect, the calculation of the “discount rate” to return 100% of the original investment.IRR = “what discount rate would one have to apply to a series of future cash flows in order to return 100% of the original investment”Goodwill technically is the difference between the book value (depreciated) of assets and the intrinsic or true value of a business.What you are suggesting is the “market value of intangible assets” like the brand, the customer lists (which is arguably not an intangible asset), etc.The residual (Year 10) value at the termination of the business is likely a negative number as it costs money to shutdown a business and it is likely being shutdown because it has failed. The creditors or investors or owners would be entitled to recover the value of any intangible assets.

i would love to tag team a class in business finance with you JLMthat would be so much fun

I’d love to sit in on that class. Take that Seth’s alternative MBA

Take a look at the Acton MBA school in Austin, TX. It is the MBA program designed by business folks for students who want to learn to make money IN business rather than learning ABOUT business. All of the instructors have been to the paywindow.

i’ll provide security

I was on the fence but if you’re going to provide security, then I will have to jump all in! LOL

I would take that class.

I think IRR works best for situations without intermediate cash flows. This is because the model contains a simplification in which it is assumed that intermediate flows can be re-employed at the same return as the IRR. For high return projects, this can lead to a major overstatement of the true return.

Agree completely.I see IRR as simply a consistent lens which calibrates vision rather than always creating clarity. Like every financial analytical technique, it should never be used alone and it should always be tested by other virtuous techniques.I think a consistent way of looking at deals or financial results within a particular industry is very useful to be able to prioritize or compare the relative merits of competing deals.

I have used Modified IRR in the past for business cases to get a more accurate picture:More here- http://en.wikipedia.org/wik…Also Fred- Is it possible to ask the Disqus folks to add support for comments via the Blackberry web browser. I wanted to comment on the day of the post but couldnt via the bberry and just remembered to do it now via my PC

I’ve been asking for blackberry browser support from disqus for a while. I would also like to be able to click on a link that says ‘comment via email’

actually that would be great…something like:email [email protected] to comment

Really? Can it be true that people reading this blog are unable to do this basic math and need help?

i don’t know. let’s see if anyone out there found this useful and informative

Fred – I found it useful, thank you.Andy – I can do a lot of math when it is set out in front of me, and make up a lot of formulas and projections, but it is always useful to see examples to confirm that I’m doing it right.P.S. The best part of the naive spreadsheet, which no one has pointed out yet, is that “invesment” is spelled wrong.

oops

I thought you were just being witty 😉

The utility comes in understanding investor expectations. Rapid back of the envelope ball parking appears to be a good shooting from the hip methodology. At least good enough to invest in folks that have gained Gotham Gal and Fred’s trust, which is much more important than the quality of the estimate.

I really like when you do posts like these. It’s second hat to you, but you never take that for granted and take the time to explain it in nice laymen terms. Thanks.Curious…Does your non-tech angel investing follow any rules from USV (1/3, 1/3, 1/3 or specific areas of concentration… i.e. restaurants)? Or is it more simply you like the people, you like the “product” and you believe it will generate some type of return while helping bring a “product” into the world you think should be there?

it’s not 1/3, 1/3, 1/3. we hope to get our money back on >75% of these investments. we also don’t expect to get rich on them.

Fred,In the Google Docs spreadsheet, is there any particular reason why you used the version of the IRR function that includes a “starting guess” argument, and why you chose 10%? You could have omitted the second argument altogether. (I think. Or maybe I just don’t understand the dark arts of finance.)Thanks.

that’s a habit from the early days of excel. it used to be that if youdidn’t put in a guess, you might not get a good result. i think that’s longbeen fixed but i still do it out of habit

You’re right more folks should know about this. However, I would recommend going beyond this model as it doesn’t take into account opportunity cost and inflation. I prefer discounted cash flows and NPV. That said, these models are really difficult to apply to any start up.

yes, you can get very complex with this stuffbut when talking about a local restaurant or community blog/newspaper, ithink this level of detail is just fine

I’m surprised you use this technique. I think an equivalently simple DCF gives a better picture. Even if you only discount for inflation, it’s great to see the PVs of the future cash flows – and if you chart them, you can almost ‘see’ the risk profile of the business.

With you on DCF; I’m a fan of generating a NPV and looking at that as “the pie”

agreed that NPV is a great metric to know and track. but i like to think in terms of returns not PVs

Sounds like David wants in on teaching the class with you & JLM. “Make it so #1”

Steady Mark! Fred and JLM are out of my league.Advising other people on investments is one thing, but having years of experience making your own puts you on a different level….

You’re still way ahead of me. I’d be cautious about using any models, just due the weaknesses of assumptions that go into them.I understand the need to have these loose frameworks, but wonder about how much faith (or time) we should sink into them.

Mark, you’re way too modest! Anyone who understands theoretical physics can pick up the basics of financial analysis in a jiffy.And just like physics, it’s important to know the underlying principles. For example, the value of *any* asset is simply the present value of the cash flows is generates over time. That’s it!If this value is higher than your outlay then you’ll make money, if it’s not you won’t. (assuming your numbers are right)That’s all there is to it – and, as you can probably already see, the hard part is getting the projections right, not how you model them.Drop me a line if you’ve got any questions.

My theoretical physics knowledge is terrible with 15 years of decay since my degree. I’m lucky me and newton are still on friendly terms (although I’m fascinated by probabilistic and waveform representations).You broke it down into essentials, as far as basic finance I’ve come to grips with the estimated future payout over cash in and depreciation. Good chatting about this topic, makes it clear I’ll need a good book keeper.

what is interesting is the number of us chatting while we review the spreadsheet – passing links and asking questions.

what is interesting is the number of us reviewing the spreadsheet and chatting while we do, sharing links and asking questions. I now know how to calculate IRR.

what is your take on calculating returns for a longer lived asset? would you throw a multiple of some earnings/cf metric at the end of the projections and include that as cf to investors? i personally try to avoid multiples if at all humanly possible, but so many people use them. to me they fall out of a valuation as a descriptive measure, should not be used to drive the valuation.

In making an accurate projection of the value of any investment, it is necessary to make some determination of the terminal value at the end of the investment time horizon.This may take the form of a positive value (you sell the business or the business assets to somebody else for a profit), a neutral value (you kick the remnants into the fire, piss on the fire and go home) or a negative value (business fails, bayonet the wounded and pay off the creditors).How you arrive at the terminal value is a business valuation exercise and any pertinent and accurate technique is fair game.Sometimes the terminal value is the real value of the investment as most of the money comes at the end of the deal when you sell it — this is typically the case for as an example real estate.

yes, you’d have to do that with real estate or some other asset that has a terminal value. that’s less appropriate for a retail or restaurant business that may not be something you can sell.

This is great. Though I need to think about it some more. I copied it so I could edit it, I can’t edit your version.So I calculated for whatever my reasons the IRR of 2010 to 2011. I’m getting a small but negative rate (-.6 repeating) This sounds logical right? This is the first time I am doing this.Also you could totally use this for other purposes..I’m just trying to figure out what…

the IRR will be negative if the capital invested hasn’t been paid back during the years you are calculating it

Good then I have been figuring this out.

There should be a spreadsheet of common “half lives” for particular businesses by industry. For example, Restaurant -7years till out of biz, 5 years till incremental 25% decrease in returns, etc.

There is — it’s called “Closed for Remodeling”!Restaurants in particular, like expensive luxury cars, are most profitable when the concept survives the depreciation of the original cost to open the business.Then the depreciation expense truly disappears and the expense is converted into a profit.Restaurants are a very, very, very risky business.

they sure are. but if you back a proven entrepreneur who has a following, it can be less risky than you think

Agreed. I am sure you have eaten @ Louie’s 106 in Austin in the Littlefield Bldg @ the corner of 6th and Congress up the street from UTIMCO.

This is useful for most of us without an MBA. Hope there’s more to come.

Is IRR really a measure of ROI though? From what I remember, the IRR (in the capital budgeting sense) is the rate that forces a NPV of 0. I think one could almost say it’s the return your need to get to break even. It serves as a tool to compare which projects to invest in.Anyways, it’s been a while since I looked at this so I could be wrong.–Marco

if your required return for this project is 10% and the irr of the cash flows is 12%, then the project has a positive npv to you. you are correct that irr is the rate that implies a 0 npv. but next step is to compare that rate to your required rate for a project with those risk characteristics to see if it achieves your hurdle.

both of you are correct

I think that the projections are just one small piece of the puzzle; and an overvalued one at that.What’s more important are the people, the idea, and your confidence in their ability to change as needed.You can analyze and analyze and try various metrics. Sometimes that’s needed and useful and helps you understand various aspects of the business. Generally though I think it’s a dangerous habit to get into. Over analysis can be the enemy of creativity and great ideas and businesses. The future can’t be solved for with projections; yet projections can limit your ability to put faith in people and great ideas.Too many people act as if projections are more than they are – best guesses. A relatively simple approach like Fred posted is plenty good in my book, with 2-3 “scenarios”. If the projections make sense and you trust the people and the idea seems smart to other smart people … well that’s what I want to see.

Kevin, let me disagree as completely as I can with your comment as it relates to the value of financial projections in the investment decision making process but more importantly in the running of successful real businesses.At the end of the day, the initial projections are simply a pre-game model for the ensuing income statement, statement of cash flows and balance sheet as well as the calculation of investment returns. The strategic, business and marketing plans of the company are subsumed in these numbers.More important they become the framework for the company’s budget and long term forecast which should be updated every 90 days (with prior 90 days performance numbers in hand) and which should be continually correllated with the company’s strategic plan.The tools available today to entrepreneurs to forecast their financial performance are easy to use and can be manipulated to create numerous scenarios to provide a bit of contextual and sensitivity analysis. Change the assumptions and weigh the differing results.The ability to transform the “idea” into numbers is critical to creating the business plan and the marketing plan which will propel the business to success.Entrepreneurs don’t like details, they usually like broad strokes. I am a numbers fiend but I truly hate them. That is why most investments require a “team” approach.Sometimes the most valuable member of the team is the number cruncher or for an operating company, the CFO. The best thing a successful CEO can have is a CFO who is conservative, who makes love to the numbers, is timely and who is not carrying a Marshal’s Baton in his knapsack. I have never, ever paid enough for a great CFO and I would be cautious in proceeding without one.An entrepreneur does not have to create the numbers but he damn sure has to know and believe in them. Cause we are all keeping score with money! You can have all the credit for our success if I can have all the money.Read a great book — “Competing on Analytics” by Davenport & Harris. I don’t consider it perfect but it sure sets the bar as to how one must use the analytics of a business to derive the competitive advantages which are necessary to fight and win in today’s business environment.All the easy deals were done in the 1960s and now everybody must be multi-dimensional and understand the numbers. Not running a business based upon its numbers would be like trying to fly a modern airplane without a GPS.

I didn’t say you shouldn’t run a business based upon numbers. I said that projections before you get started are of limited value. Once you are up and running the numbers become more important than when everything is based on assumptions, in my opinion.

Kevin, I am not peeing on your leg and cursing the rain. I have been doing this stuff since before the invention of personal computers and VisiCalc.We Americans are a lazy bunch who want to be forgiven for a lot of business sins just because we are deal making, company starting, high energy, A personality junkies.I am OK with that, just get a damn good numbers guy.Just remember there is no shortage of nice bright young men with great ideas — the question is really can they get their product to market and make a buck in the process. Can they run a business?Oh, yeah, in a predictable manner and under control.Assumptions are judgment. The quality of the judgment is the product of one’s instincts, thoughtfulness and experience. Some folks have good judgment and some folks have bad judgment. To say that it is an “assumption” is simply to acknowledge the obvious.Judgment is very, very, very case specific and subjective. And this is why it must be exposed and examined.Tiger Woods — golf judgment? GOOD! Maybe the best in the world.Tiger Woods — moral judgment? Hmm, NOT SO GOOD! Maybe the worst in the world.To use that as an excuse to avoid the rigor of making judgments, documenting them, testing them and finally championing a family of outcomes is just laziness.Good judgment the product of experience.Experience the product of bad judgment.

Great post Fred!I think it was useful in hearing your perspective and seeing the talkback. I would say that for most entrepreneurs it is not that they can not run the numbers rather, they are uncomfortable projecting numbers that are WAGs. Serial entrepreneur on the other hand have a reputation behind that lends credibility to their number even though they are usually WAGs as well.I am struggling with this issue as I write this, I can run numbers that is not my problem I have a hard time projecting a market share that is reasonable but still a complete WAG.

your revenues may well be a wild ass guess. but your expenses should not be.

I guess the cash in year should be 2009 in stead of 2010, as AVC put cash in at the beginning of 2010 (or end of 2009) and get the first payment at the end of 2010. The real IRR would be even lower than 14%.

yup

What a refreshing discussion in a “don’t write a business plan” world.

i’m not a huge fan of detailed business plans. but i do like the discipline of financial projections

Thank you, that was very helpful. I’m looking for a similarly clear explanation and template for calculating break even for a variety of scenarios. Have you written on this topic or will you?

i might. what do you mean by a “variety of scenarios”?

Fred, is this how you assess your tech startup investments too?Pleeeeease tell us that your answer is an emphatic “No”, otherwise the M&A finance world is about to have a field day with this crap you have put out.

No. Tech startups were actually invented since IRR calcs where too complicated, so we just wait for $100M exit.What is also great in tech start-up is that their cost of capital is zero, so they don’t have to do the math 🙂

first of all, no this is not how we assess our tech startup investments. we don’t even do this much financial analysis to be honest.second of all, what about this is “crap”?

ooops. sorry for replying to this. didn’t read this comment till the end.

As one with an MBA from Columbia, I can say that you would save a whole lot of first year students about 1-months tuition with this dead-simple breakdown. For some reason they insist on giving you the whole model piecemeal, so it doesn’t start coming together until late in the semester…I am not as bright as some who went before me there though, so I definitely can’t speak for everybody.

Yes, can use a spreadsheet to find ROI! Yes, have, say, one column for each time period! Yup, can do that!Then maybe want to do some more planning, say, with some additional details about the business and some business ‘decisions’ during the planning period. I mean, ‘business decisions’ are important? Right? I believe I have seen some articles on that! So, for each such ‘decision’, have a cell in the spreadsheet, in the appropriate column, and type in some guesses for the decisions.Then might like the ‘best’ decisions, say, the ones that make the ROI as large as possible. Well, commonly in spreadsheet software there’s an app for that, based on L. Lasdon’s GRG2 (generalized reduced gradient version 2)! In really simple cases can use linear programming, and people have tried that, too.Well, with those ‘best’ decisions, might notice that there may be some unknown quantities, some exogenous effects! So, for each such effect, might have a cell in an appropriate column of the spreadsheet and insert a formula starting with the random number generator.Then with those best decisions determined and fixed, can run many ‘trials’ drawing different values from the random number generator and get the distribution of the ROI, etc. Nicer. But still not very nice:Football fans would object! Even with the best decisions from GRG2 are calling all four plays on first and ten and on plays 2, 3, 4 staying with those plays and ignoring additional information available there. E.g., maybe the CFO is long some stock and short the corresponding warrants and wants to adjust each period based on what the stock and warrant prices are doing. Gee, would anyone ever think of doing such a thing?So, should not make and fix all the decisions at the beginning but should make the decisions DURING the planning interval. Software might not know that, but everyone in football and business does.How to plan the business assuming that will be making decisions the best way during the planning interval?People have thought of such things. One such person was R. Bellman. There is more inE. B. Dynkin and A. A. Yushkevich, ‘Controlled Markov Processes’, ISBN 0-387-90387-9, Springer-Verlag, Berlin.So, get the highest expected ROI possible with ‘highest’ in an especially strong, really the strongest possible, sense: Are making each decision using all the information available (that is, don’t know the future) at the time the decision is made. Or, don’t make all the decisions at the beginning but delay making each decision as long a possible but not longer!Dynkin has long been at Cornell.The field can also be called ‘stochastic optimal control’. Yes, Black-Scholes is a very small special case, a Nobel prize, etc.Yes, need more than just GRG2 here!Yes, the computing is commonly a supercomputer application or worse. It could be a way to keep busy lots of 48 core Intel processors!There are ways to make the computing faster: Can do some multi-variate spline approximations to speed up some of the computations. And R. Rockafellar, at U. Washington, one of the best workers in the field, has a cute approach ‘scenario aggregation’ where, actually, get to make use of, say, GRG2 again.So, net, get to maximize the expected ROI in the most powerful sense, making ‘best’ decisions DURING the planning interval, and also get the distribution of the ROI. That’s what we would want, right?No, it wouldn’t make a good venture funded business (yet!)!

This won’t be news to you, Fred, but for the other commentors here, I wrote a quick extension on the proper use of IRR and one of it’s potential downfalls if viewed alone. http://thegongshow.tumblr.c…

Locally we have a saying that don’t spend more than what you earn..Basically this is true in a sense ROI should be base on your expenses before projecting profit.

This works for you, because the Gotham Gal knows what is good and what will catch on and sell well. Good taste=good instincts

It’s amazing how many people don’t get this. Cheers!

this is both timely and helpful as my finance classes are a bit dim in the rear view mirror.thanks for posting, Fred!

Simple tip, yet very useful especially for startups run by developers.

This is really timely, Fred, love these kind of practical posts.As a first time entrepreneur, have always tracked cash flow religiously but since recently investing my own money in the business, I was wondering hey, what kind of return am I expecting? Things have been incredibly busy, so doing it went to the bottom of the urgent pile.The spreadsheet was simple and easy to use. Many thanks!

IRR is the wrong way to value an investment. Use PV instead.

actually, the 25% is the classical definition of ROE (profits over equity). the nomenclature they are using is not incorrect, its just not what you want to see.

Ahh good ‘ol startup economics. Thanks for sharing!It seems that you are only describing a startup that gets investment at 1 point in its life.However, it would also be very useful for startup-minded folks to see how you would like startups to make projections based on the expectation of future funding events. For example, the angel round -> series A -> series B -> series C etc. Wouldn’t you want those projections to be factored in here somewhere?

yes, you can put negative cash flows into the first row in any year youwant.i was trying to keep it dead simple to make a point

Excellent article. Every should try this before investing your money. An important financial tool.

For a startup, I don’t think it’s very useful to get involved in advanced discussions on risk free rates, expected rates of inflation, etc. Although they’re important components of financial analysis, they cloud more than they reveal for a new company.When looking at a business plan, revenue is ultimately unknowable and costs can be roughly (under)estimated. A good rule of thumb is that revenues will be half of your projections, and expenses will be double.The most important thing about a financial plan is what it says about the management. By looking at a plan you can see how well the management has thought the plan through. In most business plans, you will see a revenue guess of 25% compound growth per year to infinity. It’s completely unbelievable.In contrast, you know a QUALITY plan when you see “we plan to hire X salespeople in the first year who will be expected to sell $Y every year”. Or it could be, “we plan to spend $X on Y internet advertisements, where we expect a conversion ratio of Z”.The difference is that the management is highly focused on HOW they will sell the product. If you have a team that knows what they’re selling and why, the expenses will be of secondary importance.

What is of interest to me is the part where you humbly say the business will likely no longer be in business in about 10 years. Tastes change. The market shifts. So instead of the business being a dying star, could it be a business team that is adept at reinventing itself? Nokia did not start or even mature as a cellphone company. The Bay Area was known for fish and not chips only a few decades ago. Could that reinvention model be applied to small businesses as well? It is not like these people stop working after 10 years. They continue to work. They just go start something else. Instead of dissolving one entity and then again raising money for another, could the original entity factor in the whole thing and keep money from one operation to plough into another new one?

In this example, you show the cash in and the first cash out happening at the same time, T+0. You’d expect the first cash out to occur at T+1 (otherwise, why not just invest $300,000 at T+0?), so all of the cash out events should be time shifted forward one year. This drops the IRR down to 9% (but the multiple is still 1.3x, so multiples are a pretty meaningless number unless you know for sure that all else is roughly equal).

YesYou are right

Don’t mean to complicate Fred’s excellent and straightforward approach to calculating a return on investment, but I do think that people should look at this discussion thread to get multiple viewpoints on the merits and demerits of IRR versus other commonly used ROI metrics:http://www.finance30.com/fo…A number of very seasoned practitioners from all around the world weighed in with their experience and opinion, including investment professionals from Fortune 500 companies, college professors and senior bankers.

le mythe écorné du 25% de ROI !….

agreed. but it is easier if you have built similar businesses in the past